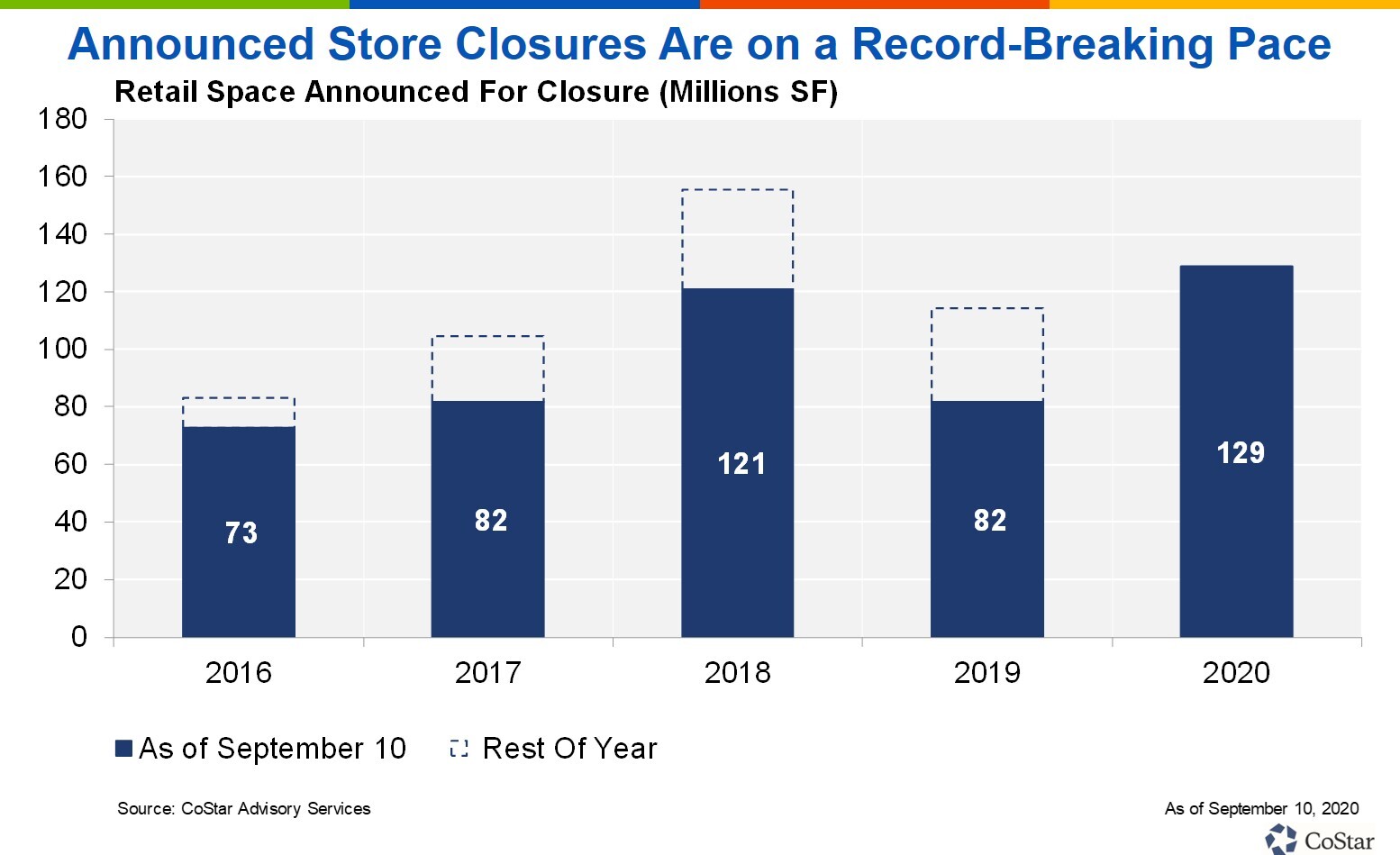

Announced Store Closures on Pace to Set Record

Fallout Not Felt Equally Across the Retail Sector

Retailers have now endured an arduous six-month stretch during which a global pandemic led to widespread lockdowns and an ensuing recession. For most, it has been a very bumpy ride. With more than three months remaining in the year, announced store closures for 2020 have already surpassed last year’s level and are now on pace to reach an all-time high.

While the pandemic will continue to have a significant impact on the retail market, digging deeper into this year’s announcements shows the effect will not be felt equally across retail tenant sizes or center types.

Year to date, retailers have announced plans to close nearly 130 million square feet of store space. In addition, more than half of this space can be chalked up to five traditional retailers: J.C. Penney, Macy’s, Stein Mart, Bed Bath & Beyond and Pier 1 Imports.

Traditional retail, largely composed of apparel and department stores, has been struggling for years as e-commerce growth has siphoned sales from the sector’s brick-and-mortar locations. The coronavirus pandemic has only accelerated this trend.

Conversely, over the past several years, experiential retail, such as restaurants, gyms and movie theaters, had proven to be a key source of growth because of its relatively low exposure to e-commerce competition. However, experiential retail has also been severely disrupted by the pandemic, and some major tenants in this sector have recently announced closures as well, including 24 Hour Fitness, Gold’s Gym, Chuck E. Cheese and many restaurants.

As these announced closures go into effect, investors may want to begin thinking about what type of retail space is most at-risk. They may also want to look at announced store openings, which can shed light on the potential ability to backfill vacated space.

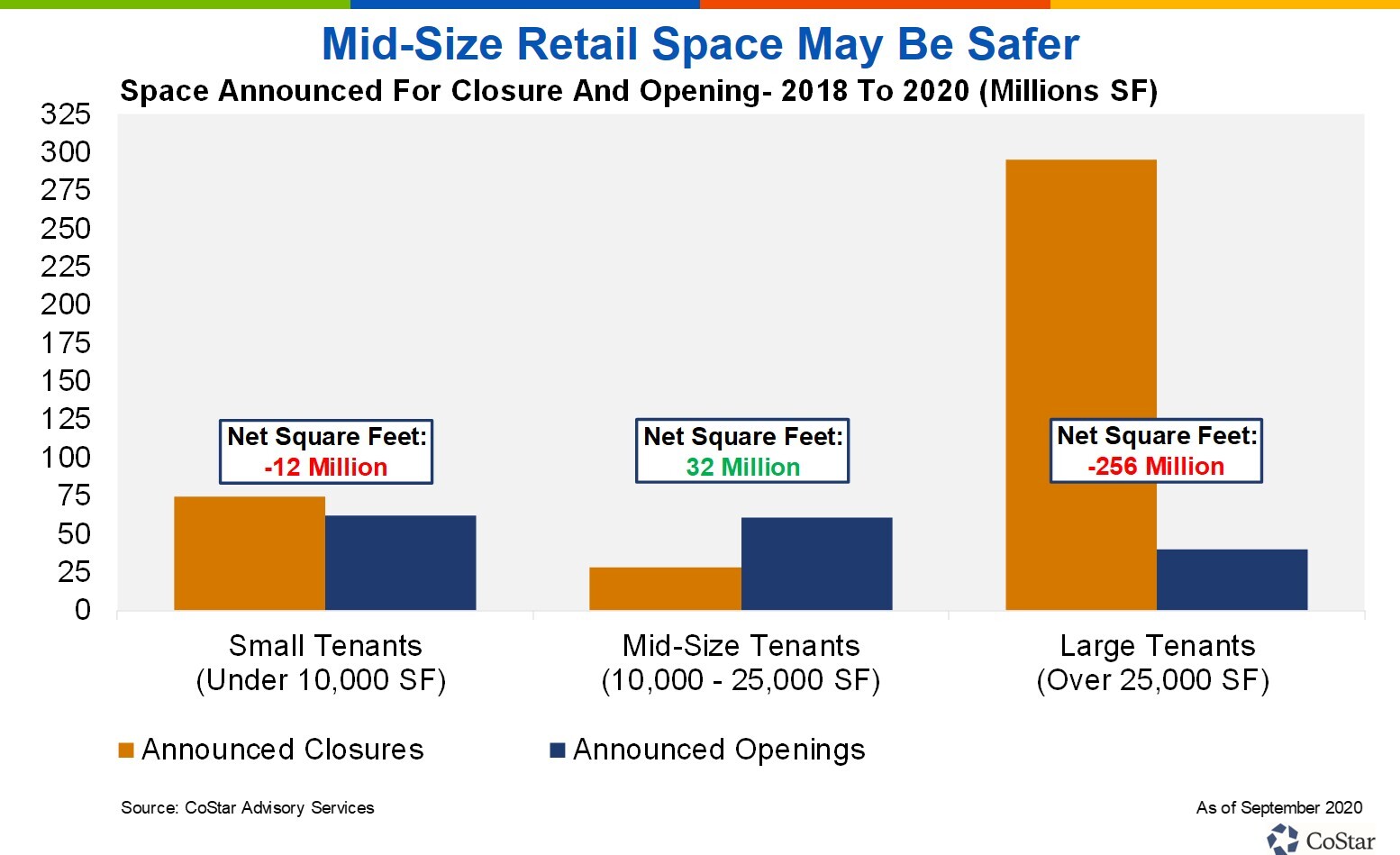

Following 2018, a year in which large anchor tenants drove closures, and 2019, a year in which smaller inline tenants were the key culprits, 2020 has fallen somewhere in between. However, one characteristic shared between all three years is that mid-size tenants have been the least impacted. This is especially apparent after layering in announced store openings.

Since the start of 2018, mid-size tenants, those with store sizes of 10,000 to 25,000 square feet, have announced plans to open about 60 million square feet and close less than 30 million square feet, accounting for a 32 million-square-foot surplus.

Over the same period, small tenants, those leasing under 10,000 square feet, were at a 12 million-square-foot deficit and large tenants that leased more than 25,000 square feet were at a 256 million-square-foot deficit.

Mid-size space may be better positioned to withstand the current disruption in the retail market and, if a closure does occur, there should be relatively more demand from other mid-size retailers to take up the space.

One caveat with announced store openings to be aware of is that discount stores have been a key driver in recent years. In 2020 alone, Dollar General, Dollar Tree, Family Dollar and Five Below have announced opening plans for more than 1,600 stores combined, and discount grocers Food Lion, Lidl and Aldi will be opening more than 180 stores combined.

Why is this is an important consideration for retail property investors? Because discount stores tend to target lower buying power trade areas and are less likely to lease space in large shopping centers such as malls.

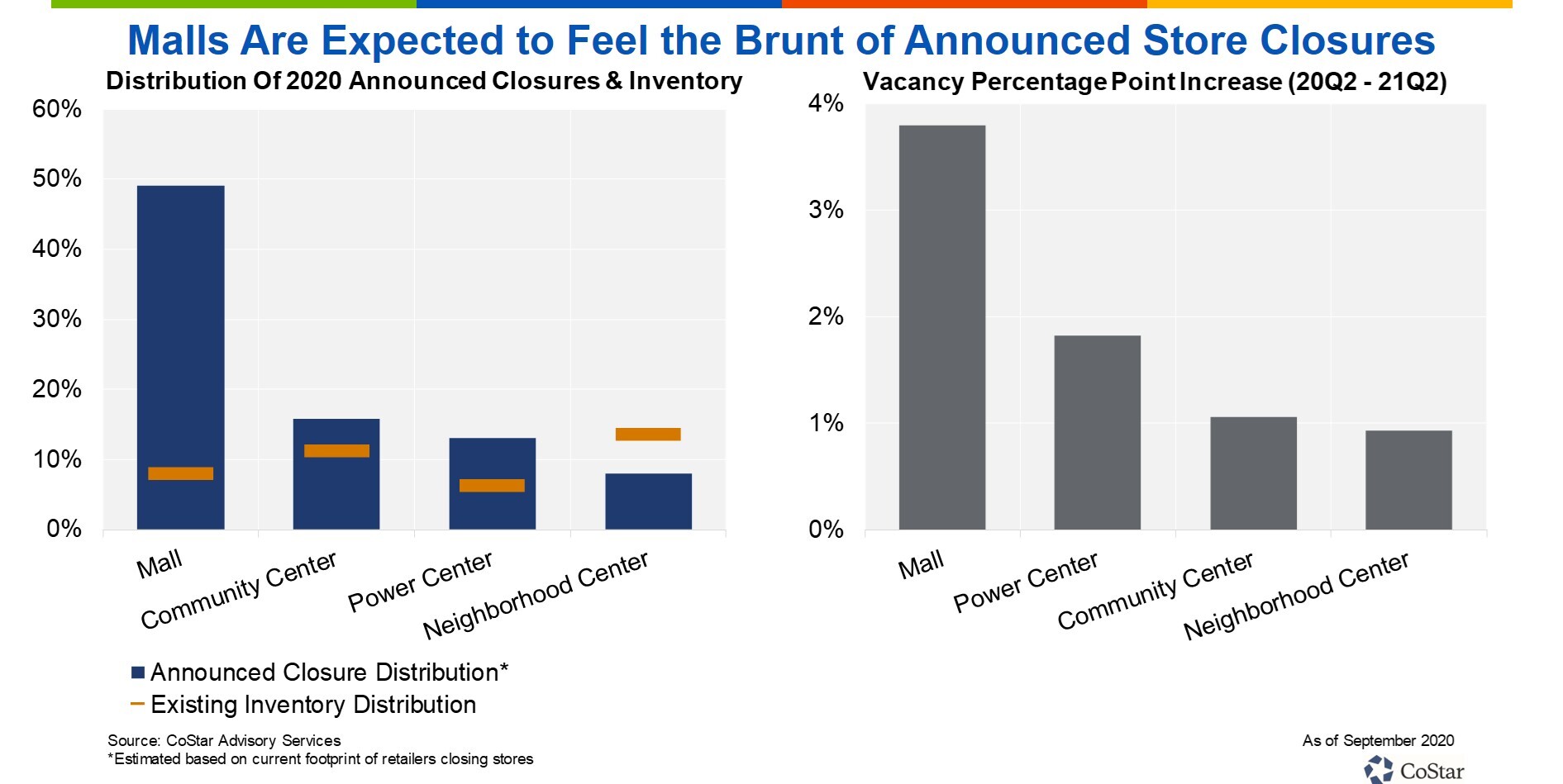

Further analysis of store closure data suggests that malls will experience an outsized share of move-outs in the near term, while neighborhood centers should hold up relatively well. The mall sector has been hit particularly hard largely because, on average, it has a high share of space leased to traditional tenants, specifically big-box anchor tenants such as JCPenney, Macy’s and Lord & Taylor. Roughly half of brick-and-mortar space operated by retailers that made closing announcements in 2020 is located within malls.

Power centers and community centers are also expected to receive more than their fair share of closures, though to a much lower degree. Meanwhile, neighborhood centers, which are typically grocery-anchored, are positioned to be relatively less impacted.

Over the next 12 months, an increase in retail vacancy will ultimately be driven by pandemic-related closures, which is why mall vacancies are projected to expand by more than double that of the next highest center type. Mall vacancies are forecast to rise from the middle of the pack, at about 5.6% in the second quarter of 2020, to the highest level for all center types, at 9.3% just 12 months later.

Seeing how announced store closures are disproportionately located in malls and not neighborhood centers, one might expect them to fare better. In our forecast, neighborhood centers are expected to experience relatively limited vacancy expansion of less than 1 percent over the same period. The forecast for power and community centers falls between the two, with average vacancy expected to increase by about 1 to 2 percent.

Retail vacancies across all center types had been trending up heading into 2020, and the pandemic will certainly accelerate that expansion over the near-term. The fact that little new retail space was being added over the past several years will help limit the impact on retail vacancy and rents overall, but investors should navigate the market with care, as store closures continue to pile up and rent collection levels remain suppressed.

As always, future retail resiliency and productivity of any given retail asset will also depend on its specific location. Research suggests that suburban retail will hold up better in the short term, but centers located in high-quality trade areas will outperform over the long term.

As a forward-looking measure, announced store closures can help put the coronavirus impact into perspective. Although 2020 is already one of the worst years on record for closure announcements, some segments of the market are positioned to better withstand this period of disruption.

Demand appears to be weak for small and large vacated spaces, which may make them especially challenging to backfill, while demand for midsize space appears to be strong enough to offset a substantial portion of its move-outs. And even as malls may face an outsize share of tenant move-outs, neighborhood centers should be relatively less impacted by store closures, which is reflected in CoStar’s forecast vacancy expansion.